Table of contents

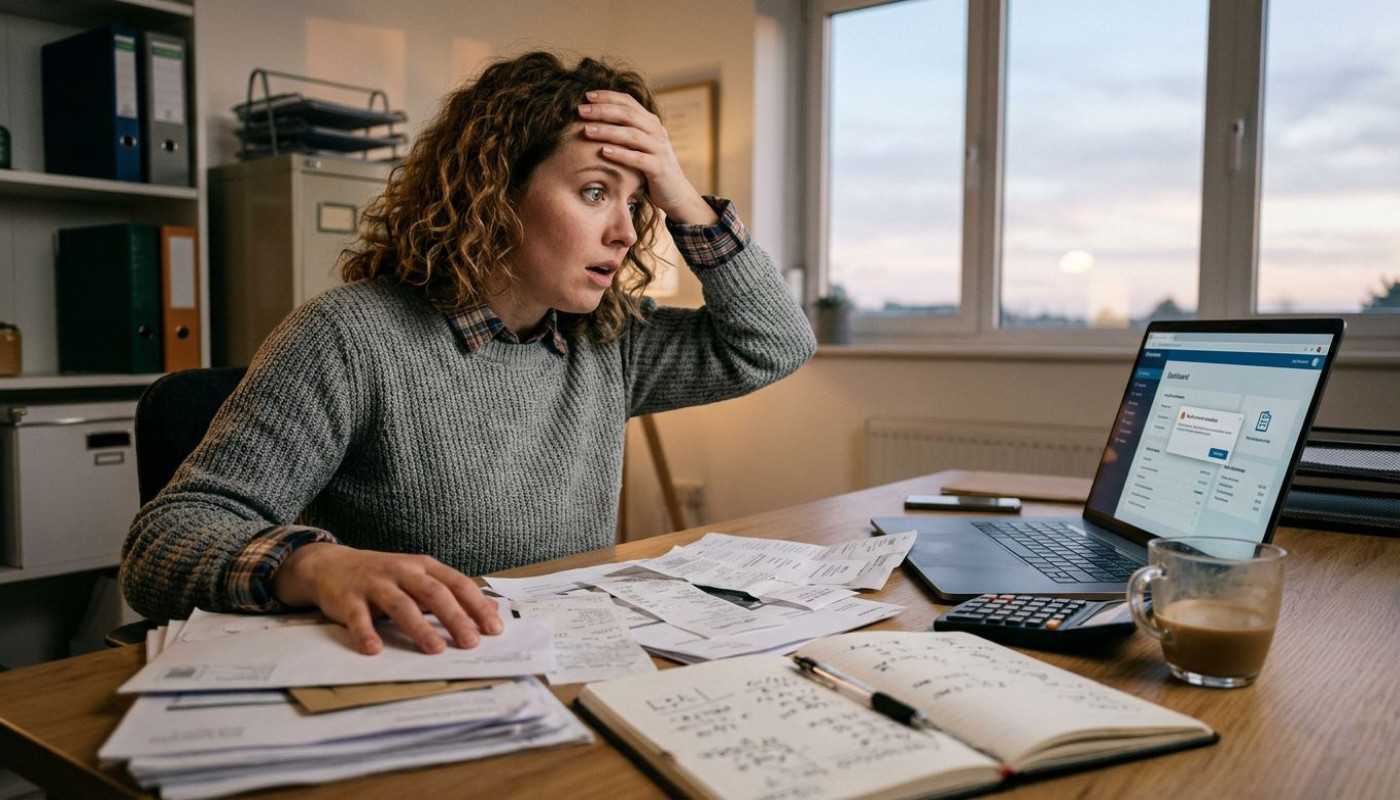

Deadlines have a way of turning “later” into “now”, and in tax compliance, that shift can be brutally expensive. In many businesses, the real risk is not the tax rate itself but the last-minute scramble: missing documents, unclear invoices, rushed approvals, and filings made under pressure. Across Asia, enforcement has become more data-driven, and finance teams are expected to reconcile payments, counterparties, and tax treatment with little tolerance for gaps. When a deadline surprises you, the cost shows up fast, in penalties, operational friction, and management time diverted from growth.

Late filings rarely stay “small”

Could a few days really matter? In practice, yes, because tax compliance is built on sequences: invoice validation, vendor onboarding, withholding assessment, internal approvals, payment scheduling, and reporting, and each step relies on the previous one being done cleanly. When the calendar catches a business off guard, teams tend to compress these steps, and what gets lost is the evidence trail: contracts are not attached, tax IDs are not verified, and supporting calculations remain in spreadsheets no one else can audit. That is exactly where disputes begin, because auditors do not assess good intentions, they assess documentation, and when documentation is recreated after the fact, it often contradicts what was booked.

The financial hit is rarely limited to the statutory penalty. Late compliance can trigger knock-on costs: bank fees for urgent transfers, external accounting time billed at premium rates, and management hours spent reviewing exceptions rather than steering operations. In larger organizations, it also creates reporting noise, because finance may need to post adjustments, reclassify expenses, or restate tax accruals to match the final filing position. Even where the amounts appear modest, repeated slippage becomes a governance issue, and it is increasingly visible in board reporting, lender due diligence, and M&A processes, where buyers often ask for evidence of timely filings as a proxy for control quality.

The hidden drag on cash flow

How much liquidity is lost to chaos? The answer is: more than the tax line suggests, because last-minute compliance tends to freeze payments. Accounts payable will often hold invoices when tax treatment is uncertain, procurement will question whether a vendor has the right registration, and finance will delay disbursement to avoid compounding an error. This pushes obligations into the next cycle, and that timing mismatch can distort working capital metrics, especially for businesses with thin margins or high pass-through costs. A few held payments can also strain supplier relationships, which matters when supply chains are already sensitive to reliability and lead times.

There is another mechanism that hits cash flow: over-withholding or conservative tax treatment taken under pressure. When teams cannot confirm whether a payment is subject to withholding, or what rate applies, they may choose the safest assumption to avoid underpayment exposure. That can protect against immediate penalties, but it can lock up funds, create reconciliation backlogs, and force the business into later refund or credit processes that are slow by design. In cross-border operations, the drag can be amplified by additional documentation requirements, translation needs, and different filing calendars, and suddenly the “tax task” becomes a liquidity problem that is measured in weeks, not hours.

Thailand’s rules punish rushed decisions

Where do errors most often start? They start at the moment a payment is prepared, because that is when teams must decide whether the amount is subject to withholding, what category the service falls into, what paperwork is required, and how to record it so that reporting matches reality. Thailand is a strong example of why rushing is dangerous: the applicable treatment depends on factors that are easy to misread under time pressure, including the nature of the service, the status of the payee, and the supporting documents that justify the chosen approach. When finance teams make these calls late, they are more likely to rely on habits, informal guidance, or last year’s assumptions, and those shortcuts can turn into compliance exposure.

For companies operating in or paying into Thailand, understanding the mechanics of withholding tax in thailand is not an academic exercise, it is a way to keep payment cycles stable and filings defensible. The practical challenge is that withholding is not just a calculation, it is a workflow: vendor data must be correct, invoices must be mapped to the right tax category, certificates and forms must be handled on time, and internal stakeholders need clarity on who owns each step. When those pieces are assembled early, compliance becomes routine, and when they are assembled at the last minute, businesses risk misclassification, missing documentation, and corrections that can take longer than the original work.

Turn panic into a repeatable checklist

Want fewer deadline surprises? Start by treating tax compliance as an operational system rather than a monthly fire drill, because the best control is not heroic effort, it is predictability. High-performing finance teams typically build a calendar that is backward-planned from statutory dates, and they align it with procurement cutoffs, payroll schedules, and payment runs, so that tax decisions occur before money moves. They also standardize vendor onboarding, require tax identifiers and contract summaries up front, and define a short list of invoice descriptors that trigger review, which reduces judgment calls made under time pressure.

From there, the aim is to make exceptions visible early. That means maintaining a live dashboard of invoices awaiting tax classification, flagging cross-border payments and first-time vendors, and requiring sign-off on ambiguous categories at least a week before filing or remittance deadlines. Many businesses also reduce risk by keeping a documented position paper for recurring payment types, updating it when guidance changes, and training accounts payable staff to recognize patterns that require escalation. None of this removes the need for technical expertise, but it does ensure that expertise is applied where it matters, and with enough time to verify documents, reconcile totals, and produce a filing that stands up to scrutiny.

What to do before the next deadline

Reserve time in your calendar now, and set internal cutoffs that precede statutory dates by at least a week. Budget for periodic reviews, especially if you add new services, new jurisdictions, or new vendor types, and ask your finance team to map every recurring payment to a documented tax treatment. Check whether any reliefs or administrative supports apply, and keep the required paperwork ready, because deadlines reward preparation, not urgency.

On the same subject

Navigating Founder Fatigue: Leveraging Corporate Support Services For Sustainable Growth

Tva Puzzle: How Small Compliance Missteps Snowball Into Big Issues

Top 3 best finance jobs

Successful investment: how to go about it?

What are the steps to apply for your first loan?

3 tips for better organisation and financial management