Table of contents

Stamp duty dominates the headlines, and mortgage rates still set the mood, yet for many first-time buyers the budget blowout starts in quieter places, during the paperwork-heavy weeks between offer and settlement. In Australia’s hotter metro markets, delays, extra searches, contract surprises, and “just one more” legal request can turn a neat spreadsheet into a moving target. Conveyancing is often treated as a box to tick, but it is also a cost centre, a risk filter, and sometimes the difference between a smooth settlement and an expensive scramble.

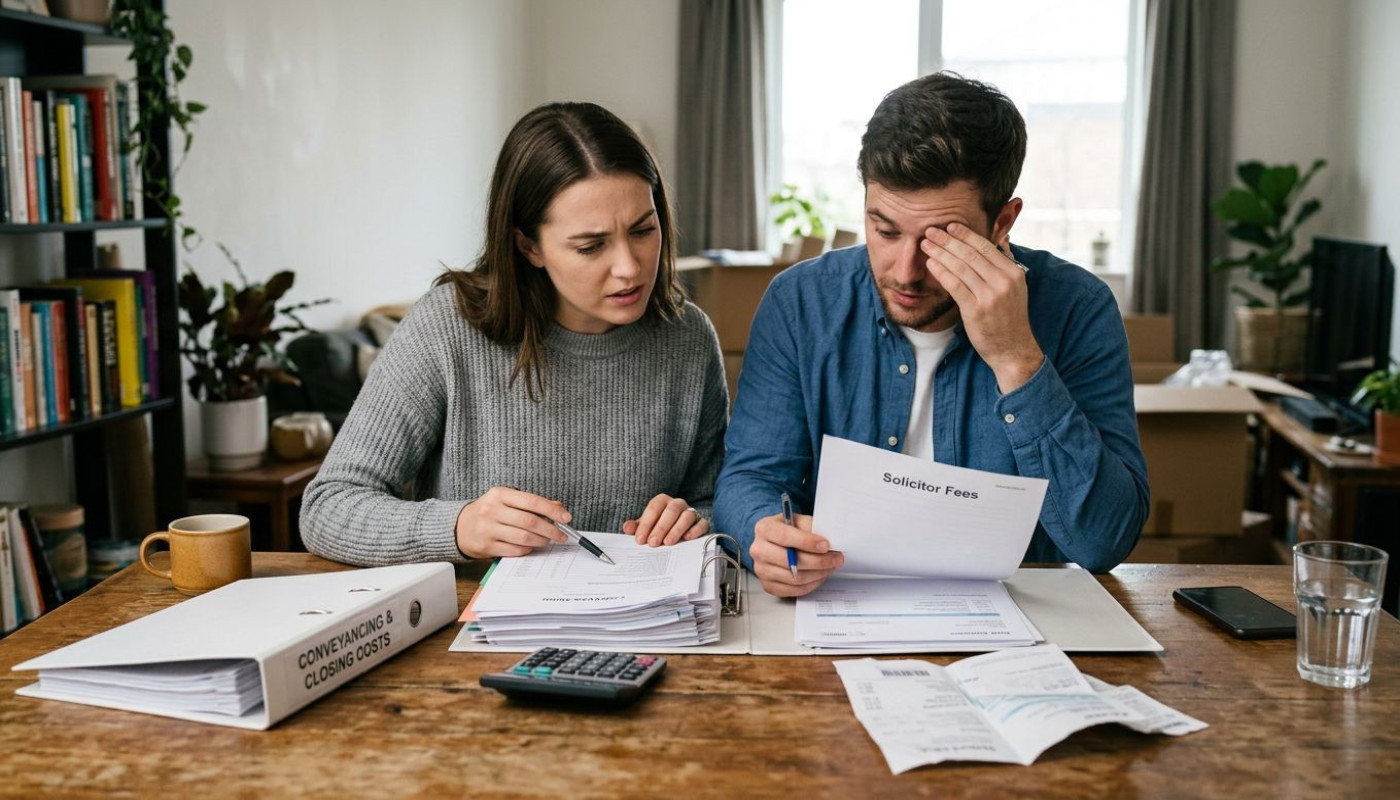

Budget shock often starts after the offer

How expensive can “the legal bit” be? Many first-time buyers plan carefully for the deposit, lender’s fees, building and pest reports, and moving costs, but underestimate the way conveyancing-related decisions can ripple through the budget once the offer is accepted, because the transaction enters a phase where time, compliance, and coordination become financial variables. A delayed settlement can mean extra rent, bridging arrangements, storage, and rebooking removalists, and while each item looks modest in isolation, they compound quickly when timelines slip.

Several common triggers sit in plain sight. Contract reviews can uncover special conditions, missing disclosures, or title issues that need rectifying, and that can prompt additional searches or negotiations; strata properties add another layer, with by-laws, levies, and records that may require closer examination. Buyers also face a choice about cost certainty: some providers quote a base figure and then add disbursements and “extras” as the file becomes complex, which can be hard to forecast if you have never settled a property before. In that context, fixed-fee structures have gained attention in major cities; in Sydney, for instance, information about fixed-fee conveyancing is increasingly sought by buyers who are trying to lock down costs early, and resources such as yourmoveconveyancing.com.au reflect that demand for clearer pricing signals.

Hidden costs: searches, strata, and surprises

Small line items, big total. Conveyancing rarely consists of a single fee, and first-time buyers are often surprised by disbursements, the out-of-pocket costs paid to third parties for mandatory checks and documentation, because these vary by property type, state requirements, and lender expectations. Depending on the deal, you may encounter title searches, council and water rates checks, planning certificates, and other enquiries designed to confirm what you are buying and what risks attach to it, and while each search may be priced as a manageable add-on, the bundle can add meaningful weight to the settlement bill.

Strata purchases tend to be a particular trap for under-budgeting. Beyond the obvious strata report, there can be follow-up questions prompted by the minutes of meetings, upcoming capital works, insurance arrangements, building defects, or disputes between owners, and each query can extend the timeline or require extra legal time. Off-the-plan contracts can generate their own costs through long settlement horizons and variations, and buyers may need additional advice when inclusions change or registration dates move. Even for straightforward houses, the “surprise” can be administrative rather than structural: missing signatures, incorrect names on documents, last-minute lender requirements, or identity-verification steps that must be completed precisely and on time, and failure here risks fees for urgent rectification or delayed settlement.

Delays can cost more than legal fees

What does one extra week really cost? In a tight rental market, a settlement pushed back by even a few days can force buyers to extend leases, pay break fees, or juggle short-term accommodation, and in metropolitan areas those stopgap costs add up fast. Removalists often charge for rescheduling, storage companies bill by the week, and employers rarely cover the productivity hit of taking multiple days off to coordinate handovers and utilities, so the financial impact of delay is broader than the invoice you receive from a legal service provider.

There is also the less visible cost of stress-driven decisions. When timelines compress, buyers can feel pressured to waive checks, accept suboptimal terms, or rush funds transfers, and each of those choices can create downstream risk. Lenders may impose strict conditions around document timing, insurance, and final inspections, and if anything falls out of sequence, additional fees can follow: urgent bank cheques, reissued documents, or expedited searches. Sellers, too, may enforce contractual rights if deadlines are missed, and while penalties and interest are not inevitable, they are part of the risk landscape first-time buyers should price in, particularly when purchasing with narrow cash buffers.

Cost certainty is a strategy, not a detail

Certainty beats optimism, every time. A first-time buyer’s budget is typically built on best-case assumptions, and that is understandable, because the process is unfamiliar and the emotional focus is on winning the property rather than administrating the transaction. Yet the most resilient budgets treat conveyancing as a planning lever: not only a service to complete paperwork, but a framework for controlling variance, reducing surprises, and keeping the settlement timetable realistic. That begins with asking direct questions before you commit: what is included in the fee, what is charged as an “extra,” which disbursements are likely for this specific property, and what timeline risks are common in the local market.

It also means aligning the conveyancing process with the rest of the deal. If you are buying a strata apartment, factor in the time required to obtain and interpret records, and do not assume the fastest turnaround; if you are buying at auction, accept that deadlines will be tighter and that pre-auction review becomes more important, because there is no cooling-off in many cases. Where possible, build a contingency buffer for settlement volatility, not just for interest rate changes, and treat it as non-negotiable. Finally, consider how pricing models influence behaviour: a quote that looks low upfront can become higher when complexity emerges, whereas clearer, all-in structures may help you forecast better, even if the headline figure appears less aggressive. The point is not to chase the cheapest line item, but to reduce the probability of cascading costs.

Before you sign: three practical moves

Build a settlement buffer: set aside funds for disbursements, document reissues, and at least one week of “life costs” if settlement shifts, because that is where many first-time buyers get squeezed.

Stress-test your timeline: book removalists with flexibility, keep rental arrangements adaptable where possible, and confirm lender document requirements early so you are not paying for urgency later.

Ask for itemised clarity: request a written breakdown of what is included, what is excluded, and typical disbursements for your property type, then compare offers on total expected cost, not just the headline fee.

On the same subject

3 tips for better organisation and financial management

What are the steps to follow to produce an excellent financial budget?